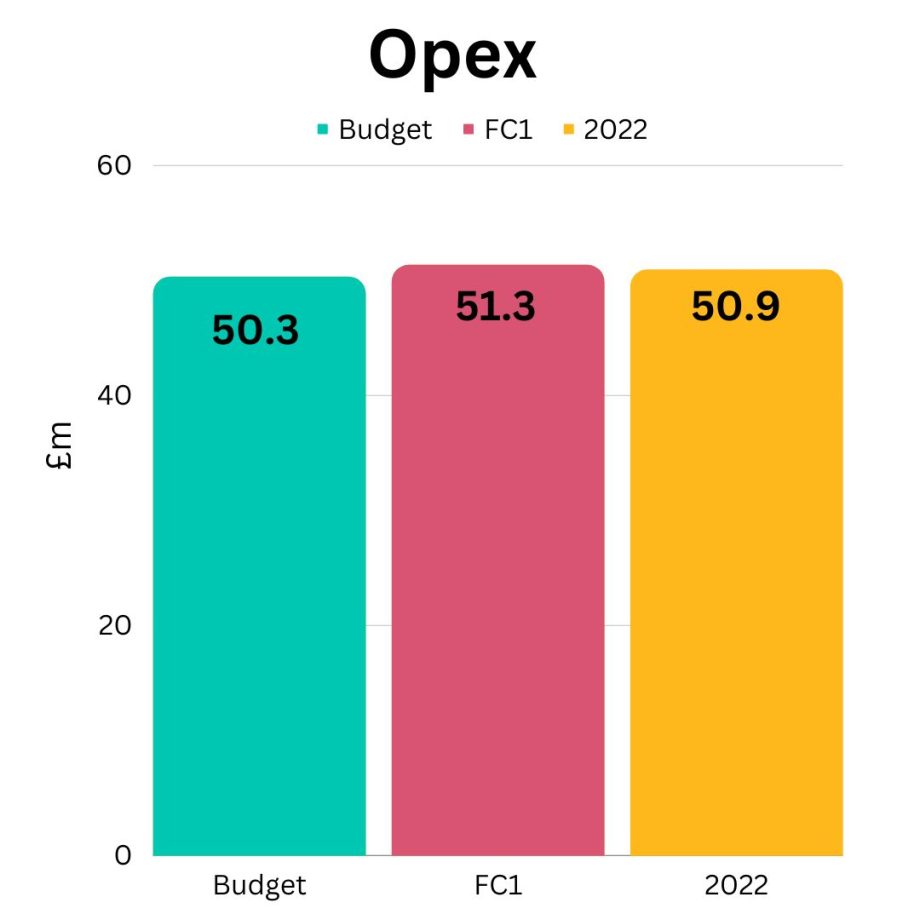

There have been some positive developments to report in the areas of freight, raw materials, manufacturing, and distribution. Our Purchase Price Variance (PPV) in freight and raw material have been favourable, contributing to overall cost savings and improved financial performance.

Furthermore, fixed costs are lower across our manufacturing and distribution sites in response to low factory and logistics utilisation, though this reduction does not fully compensate for the impact of low manufacturing and distribution volumes.

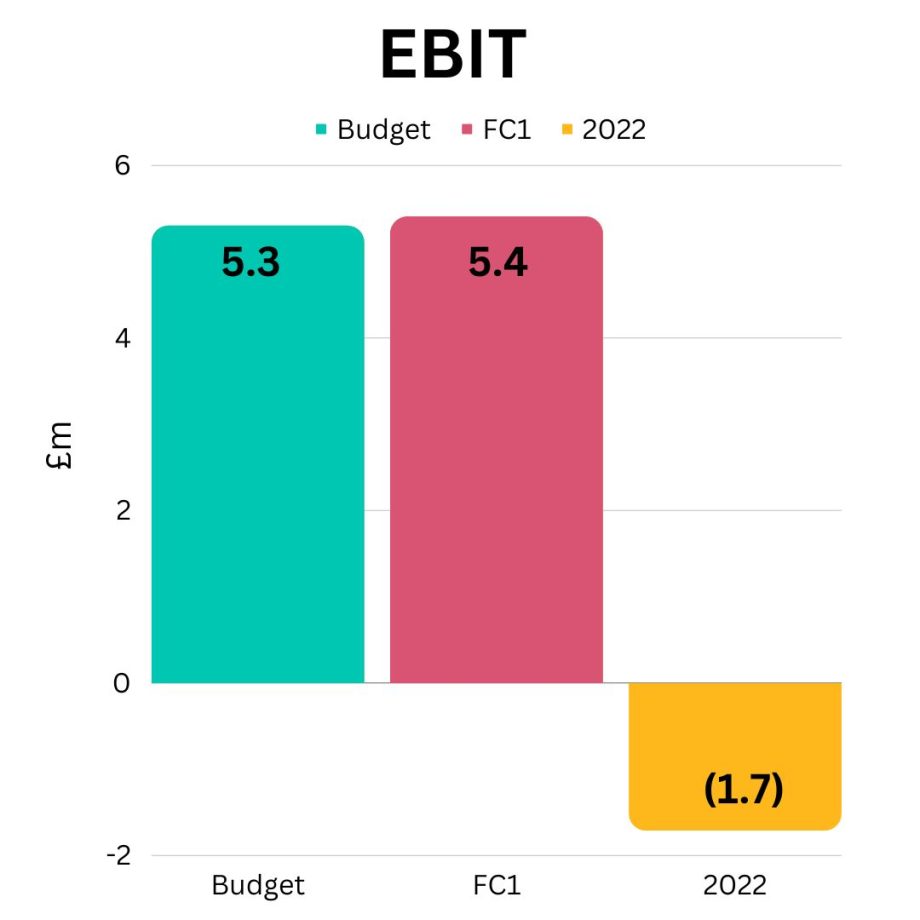

By optimising our operations, continuing to implement cost-saving initiatives and optimising resource allocation, we aim to maximise efficiency, improve profitability, and therefore position ourselves for success in a challenging business environment.